In just 2 years, the number of states where women pay more than men has doubled.

Women now pay more than men for car insurance in 25 states (despite men being riskier)

Table of contents:

Feel like you should be paying less for car insurance? Compare quotes for average savings of $440/year.

About

Most drivers don’t know it, but men and women pay different rates for car insurance in most states.

It’s a long-standing practice that’s gaining new attention now that California, as of January 2019, has banned the use of gender in car insurance pricing. It joins Hawaii, Massachusetts, Pennsylvania, North Carolina, and Montana among states that don’t allow it.

Gender-based pricing has generally been accepted by government regulators because insurers have been able to show, for example, that male teen drivers are statistically far more likely to crash and file claims than female teens, so they should have to pay more for insurance.

But California’s insurance regulator questioned this rationale last year after finding that the price differences between men and women varied widely from location to location and insurer to insurer. Some insurance companies found men more likely to file claims — thus charging them more — while other companies found the opposite. “Gender’s relationship to risk of loss no longer appears to be substantial, and the logical justification … has become suspect,” the California Department of Insurance said in its announcement of the change.

An analysis of national rates by The Zebra finds that cost differences between men and women also vary widely across the country.

Key Findings

1. Women pay more for car insurance in 25 states, an amount that has doubled since 2016.

2. Studies show that men exhibit riskier driving behavior, and they’re more likely to be involved in fatal crashes.

3. Exploring: Is gender still relevant in car insurance pricing?

Key Finding 1

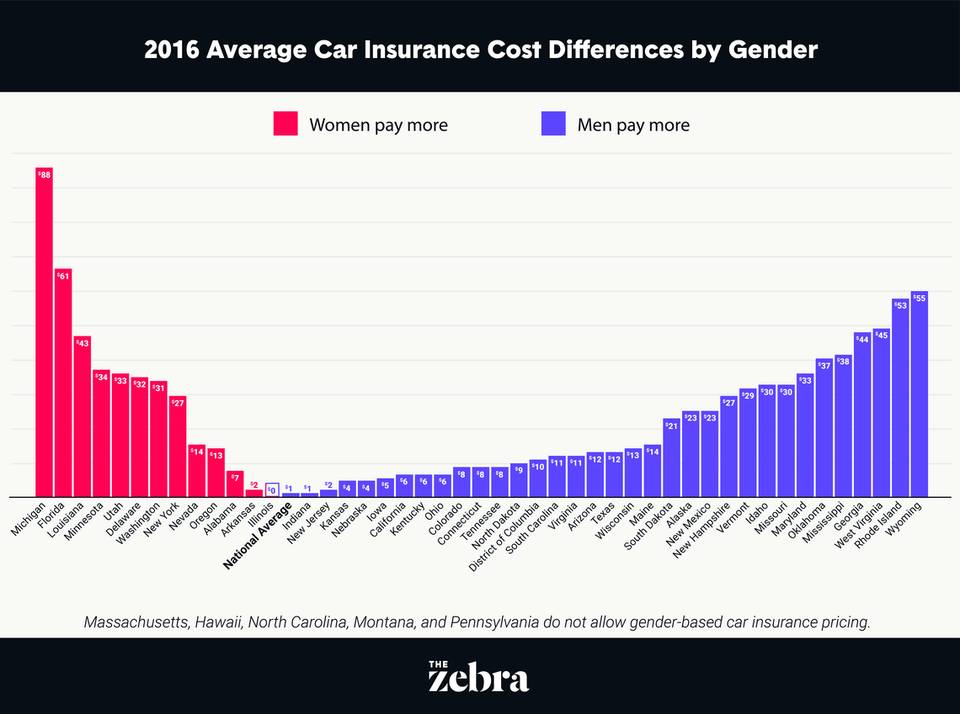

Women Pay More Than Men For Car Insurance in 25 States

Nationally, women’s average annual car insurance premiums* were about $10 higher than men’s in 2018. Women paid more than men for car insurance in 25 states, while men paid more than women for car insurance in 21 states.

Just two years earlier, in 2016, men were paying about $1 more than women on average, nationally. Men paid more than women in 33 states and women paid more than men in just 12 states. Rates were the same for men and women in Illinois and in the five states (Massachusetts, Hawaii, Montana, Pennsylvania, and North Carolina) where gender-based pricing is prohibited.

A comparison of rates from 2016 and 2018 shows that the cost disparity in many states where women pay more is growing.

Key Finding 2

Men Exhibit Riskier Driving Behavior

Our analysis shows that car insurance costs are shifting broadly for women in many states — but it’s unclear what’s causing this change.

If women’s car insurance costs are going up, it suggests insurance companies are finding that women are riskier to insure (they’re filing more claims — or those claims are more expensive). Yet, according to IIHS, “Men typically drive more miles than women and more often engage in risky driving practices including not using safety belts, driving while impaired by alcohol, and speeding. Crashes involving male drivers often are more severe than those involving female drivers.”

A closer look at the numbers shows:

– Men accounted for 71% of driver fatalities in crashes in 2017, according to IIHS.

– Men and women engage in distracted driving at the same rates, according to California’s Department of Insurance. Insurers in the state identified distracted driving as “one of the primary drivers of increased accident frequency and severity.”

– In 2017, alcohol-impaired drivers were involved in one-third of all fatal car crashes — and most of those drivers were men. According to NHTSA, there were four male alcohol-impaired drivers involved in fatal crashes for every female alcohol-impaired driver (8,022 versus 1,944).

– Speeding was a factor in 28% of male driver deaths and 18% of female driver deaths in 2017, according to IIHS.

– While most studies show men more often exhibit in risky driving behaviors, a 2011 study by the University of Michigan showed that women were more likely to be involved in certain types of crashes, especially when turning at intersections.

Key Finding 3

Is Gender Still Relevant in Car Insurance Pricing?

While 45 states still allow price differences between men’s and women’s car insurance, the practice has become increasingly controversial.

Who’s for it?

Car insurance companies have generally argued in favor of keeping gender as a rating factor because, they say, it helps them more accurately price risk.

Insurers consider gender in combination with many other risk factors (like what kind of car you drive and your years of driving experience) when pricing insurance.When states prohibit rating factors like gender, it doesn’t mean the extra cost insurers charge certain groups disappears. It just gets distributed in a different way.

In California, for example, Department of Insurance analysis shows that eliminating gender could give the riskiest group — young male drivers with fewer than three years of driving experience — a 5 percent break on their insurance costs while less-risky young female drivers could end up paying more.

Who’s against it?

Consumer advocates, however, have become increasingly vocal about the cost disparities highlighted in this report and by previous consumer studies. They argue that if gender were strongly tied to how likely men and women are to file a claim, we’d see more consistency across insurers and locations. They say that wildly varying rates are unfair, and that it’s time for men and women to just pay the same.

Consumers concerned about the impact of their gender on their car insurance costs can shop around for an insurance company that doesn’t consider gender when setting rates — or one that rates their gender more favorably.

Industry trade groups have disputed previous consumer studies showing that women are charged more than men, but they have not shared alternate data or explained why female drivers may see higher prices in some states.

Want to learn more?

Check out our guide to Male vs Female Car Insurance rates for more information as well as tips and tricks for saving money.

Methodology

*Rate data is based on The Zebra’s analysis of 61 million car insurance rates across all U.S. zip codes including Washington D.C. conducted between September and December 2018 and between May and June 2016. The analysis uses a consistent base profile for the insured driver: A 30-year-old single male driving a 4-year-old Honda Accord EX with a good driving history and coverage limits of $50,000 bodily injury liability per person/$100,000 bodily injury liability per accident/$50,000 property damage liability per accident with a $500 deductible for comprehensive and collision. The driver’s gender was changed to female to obtain rate differences.

Stay in touch and subscribe!

Get advice, insights and tips from our newsletter.