In 2021, more people were back on the road, and it appears more people were behaving badly. This trend is continuing into 2022 — and as seen in a new study by The Zebra — it’s having a big affect on their car insurance rates.

The National Highway Safety Administration (NHTSA) estimates that 42,915 people died in motor vehicle crashes in 2021. That was a 10.5% increase from 2020 — the highest jump they’ve ever recorded. This makes sense given there was also a significant increase in miles driven during 2021, as much of the country was shut down then. In 2022, the trend continues. For example, in March of 2022 the estimated number of motor vehicle deaths was up 3% compared to 2021 (and up 25% from 2020).

What’s causing these numbers to rise? Behavioral research by the NHTSA shows that speeding and traveling without a seat bell both remain higher than before the pandemic. They believe people relaxed habits during the lower-traffic periods of lockdown, and have continued these reckless driving habits even as traffic has picked back up. Speeding is a factor in approximately a third of all traffic-related fatalities.

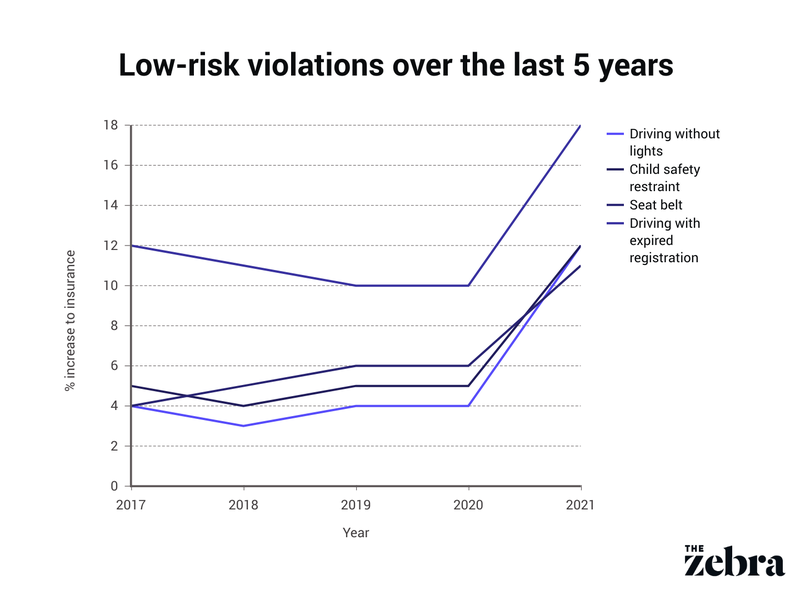

Beyond the obvious issues of making the roadways more unsafe for themselves and other drivers, traffic violations will also cause your insurance rates to rise. Insurance companies take all driving violations into account when calculating the cost of policies every year. If someone happens to be ticketed for a driving violation, they could see their car insurance costs rise from anywhere between 2% to a whopping 70% ($31-$1,077) on average. Plus, driving violations typically stay on a person’s driving record for at least three years, which means they’ll be paying the rate hike for a while.

The amount drivers pay for breaking traffic laws depends on the violation and which state they live in. A new rate study by The Zebra reveals the impact driving violations have on car insurance and what steps drivers can take to reduce that impact.