Starting the due diligence process

Your realtor is your guide through the home-buying process, including due diligence. Laws and closing timelines regarding due diligence differ from state to state. It’s the realtor’s job to keep you informed on your state’s requirements as well as what to do should any issues arise. They should also give you a rundown of what is expected for you to complete during due diligence — from understanding the contract to the various inspections. Continue reading for a list of each step of the due diligence process.

1. Check out the area

Before submitting an offer, there are a few due diligence items to work through to ensure this is the neighborhood for you, including:

- Researching the address to check for any unusual history

- Checking into crime rates for the general area

- Driving by at different times of the day to see the neighborhood activity and noise levels

- Exploring the proximity to stores, doctors and more

- Understanding the homeowner association (HOA) fees and regulations

- Researching school districts if you have or plan to have children

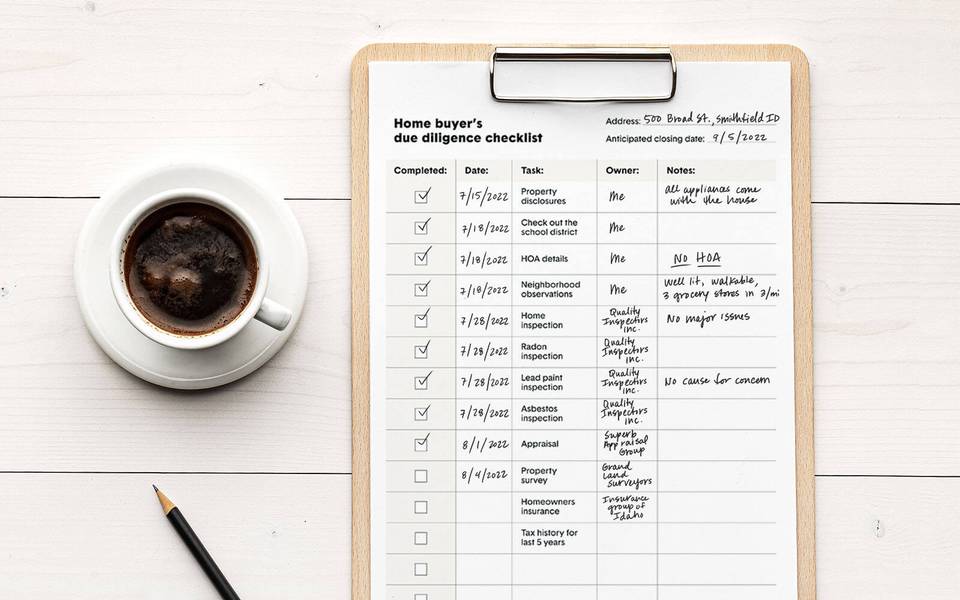

2. Understand the property disclosures

As mentioned, sellers are required to disclose any known defects or facts that could negatively affect the home. Property disclosures are written within the listing papers to which a buyer's agent has access. A few examples of what you might find within property disclosure statements are pest infestations, appliance issues and water issues in a basement.

As a buyer, you want to make sure you understand these disclosures entirely. It’s no easy feat to hold the seller liable should you find any undisclosed, nonobvious issues after moving into the property. In some states, the seller may have no obligations for undisclosed issues. In other states, you may have to prove that the seller intentionally hid these issues.

In the property disclosure statements, a section may be added to include specifics of what is included in the sale, like appliances or play sets, and any work the seller plans to do prior to closing, like emptying a septic tank.

3. Hire an inspector

Perhaps one of the most important parts of buyer's protection during the closing, inspections are meant to help buyers avoid buying a lemon house. However, inspections are typically optional unless a lender requires it, and adding an inspection contingency may make you look like a less attractive buyer if others are waiving these contingencies.

Upon receiving a home inspection report, buyers can choose to continue with closing as is, request repairs, negotiate the offer price or back out of the sale altogether. For some mortgage types, like a VA loan or a Federal Housing Administration (FHA) loan, an inspection and passing report is required to proceed with the mortgage application. Weigh the pros and cons before waiving any of the following inspections.

Home inspection

A basic home inspection analyzes the general condition and overall safety of a house. A licensed inspector will evaluate the entire property, including the exterior and interior structure, electrical systems, appliance and waterline function, grounds and more.

Radon gas inspection

Buyers can opt for further inspections, such as a radon gas analysis. Radon is a radioactive gas released from radium decay in the soil. It's colorless and odorless but is the second leading cause of lung cancer. Although it's naturally occurring, preventative measures, such as increasing airflow and ensuring proper door seals, can mitigate the radon levels inside a home.

Asbestos inspection

Another dangerous material often found in older homes is asbestos. Asbestos is not currently banned in the U.S.; however, it is not commonly found in building materials today. Asbestos raises cause for concern due to its link to lung cancer and mesothelioma.

Asbestos was often used in building materials for strength and to provide heat insulation and fire resistance. It can be found throughout older homes — in flooring, shingles, insulation, paint and joint compounds, furnaces, gas fireplaces and more. Removing asbestos must be done by a professional as it is a microscopic particle that, once unsettled, can be easily inhaled through the contaminated air.

Lead-based paint inspection

In 1978, the federal government placed a ban on lead paint for consumer use after it became apparent that the paint was causing lead poisoning in children. You can expect homes built prior to the ban to contain some lead paint; however, it’s likely covered by years and layers of non-lead paint. Once covered, the cause for concern is significantly reduced. However, action should be taken in areas with deteriorating paint. Lead-based paint inspections assess the level of concern regarding potential lead poisoning in older homes.